Stocks had a big bounce back for the week of June 8 with the S&P 500 rising by over 4.4%, and pulling the index back to 2,873. The big question I’m sure that is on everyone’s mind is what happens next. At this point, I continue to believe that the stocks will rise from here — especially given this interest rate environment, with the 10-year yield around 2%. Currently, there isn’t enough evidence to suggest a recession is likely in 2019 or 2020 either.

S&P 500 Earnings

I am modeling earnings of $165.17 per share in 2019 for the S&P 500 at the mid-point of the range. It leaves the S&P 500 trading at 17.4 times 2019 estimates. However, the forecast for next year is for earnings to grow 11% to $183.31. My model is running slightly lower than S&P Dow Jones estimates of $185.10. In the current worst-case scenario, which is one standard deviation below my current forecast, I am modeling for earnings next year of $173.30. In the worst case scenario, it leaves the S&P 500 trading at 16.5 times 2020 estimates. It would suggest to me that at its current valuation, the S&P 500 is likely fairly valued should earnings continue to fall. It also tells me that stocks are still cheap given that we are not in the worst case scenario at this point.

Dollar Sinking?

One must remember there are many things happening on a macro level that may also favor earnings growth going forward and that may act as tailwind –the dollar. The dollar has started to slip, and currently, the market appears to be pricing in 3 rate cuts over the next 6 to 9 months, based on the CME Fed Funds Watch. That will most likely sink the dollar versus currencies like the yen and euro, and emerging markets. It will make US goods more competitive and act as a significant tailwind for these companies revenue and earnings.

The dollar index is now on the cusp of a significant breakdown.

That should help to boost the price of oil and other commodities. Those higher prices should help to increase revenue and profits and lift those earnings estimates for the sector and overall market.

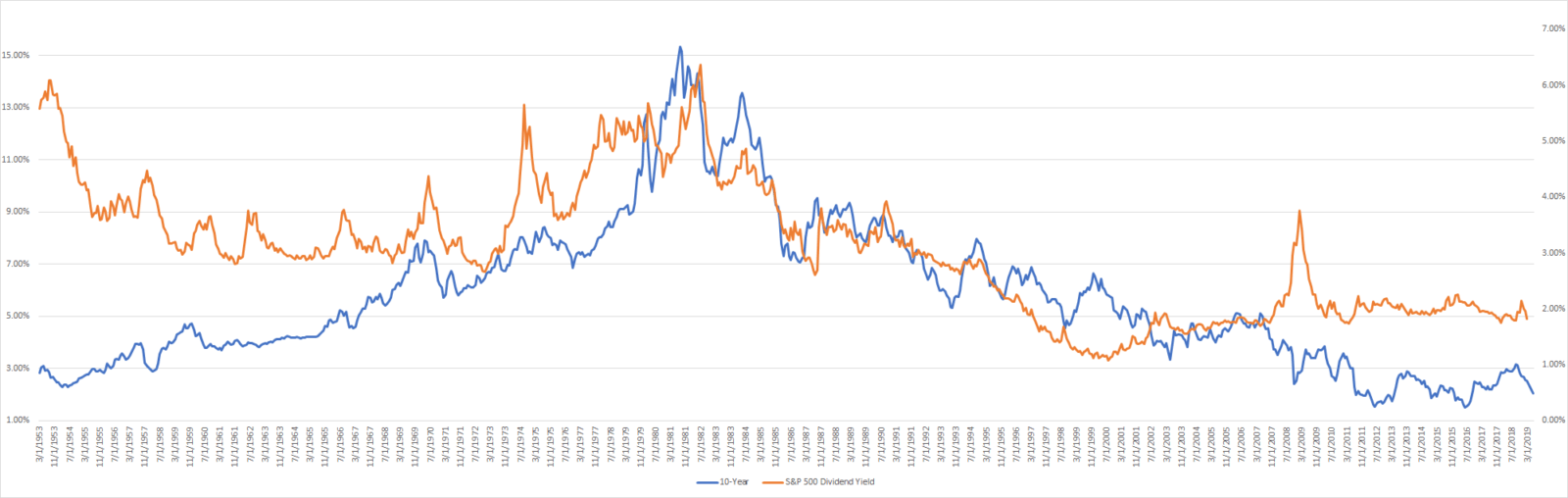

Falling Yields

One other way of thinking about the interest rate environment and stocks is through yields itself. Since the early 1950s, the direction of the 10-year Treasury yield and the S&P 500 Dividend yield have followed one another, as the chart below shows. The lower interest rate environment could result in the S&P 500 dividend yield being dragged lower as well, which in turn would send the price of the index higher.

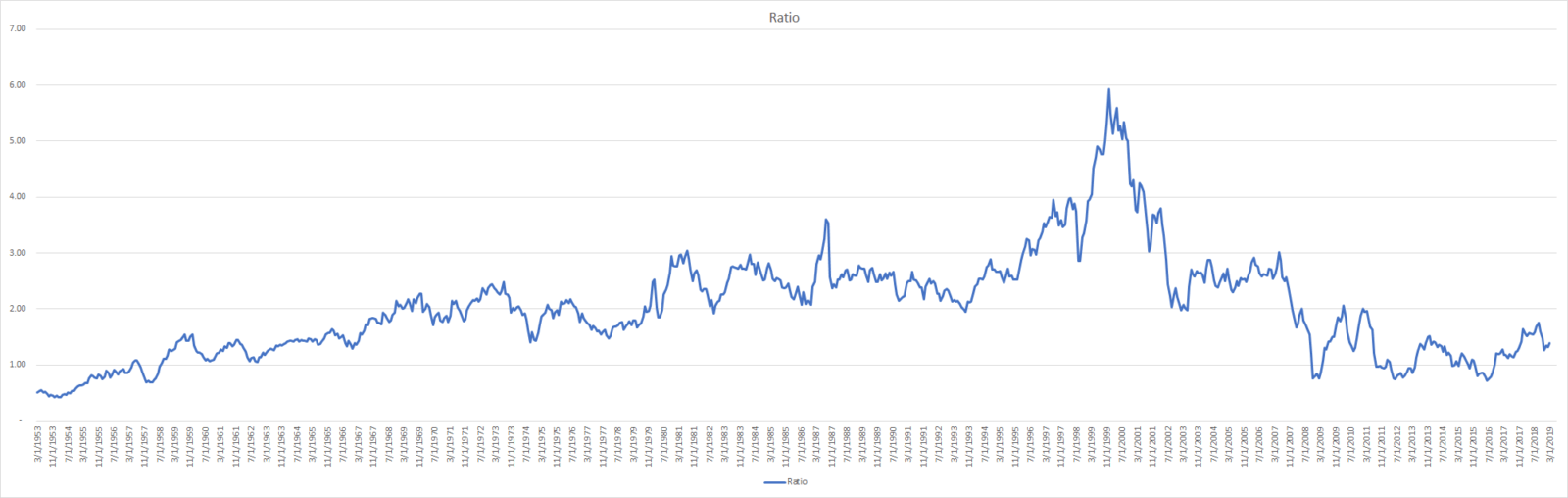

Rates To Stocks

Taking it one step further, I created a ratio that measures the 10-year rate to the S&P 500 dividend yield. Using some fundamental principals, we can determine valuation based on key events in the past. First, we know that in the late 1990s, the equity market developed a bubble, and based on the spike in the chart tells us that equity prices were overvalued to treasury rates. Meanwhile, we know that in 2008 and 2009, the equity market was plunging, meaning that bond became overvalued to equities. It would suggest that once again, bonds are overvalued to equities.

Based on the lower interest rate environment globally, it would seem that equity prices are undervalued to bonds once again.

-Mike

Mott Capital Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Past performance is not indicative of future results.