July 21, 2021

STOCKS – RSP, XLF

MACRO – YIELDS

Mike’s Reading The Markets (RTM) Premium Content – FREE 2-WEEK TRIAL

- RTM Morning – Removing NFLX From Idea List

- RTM – Growth Is Slowing And Multiples Need To Moderate

- RTM Morning: The Perfect Storm

- RTM Video- The Stock Market May Be Ready For A Big Sell-Off

It is about a week since I last touched base. Things are good here. The surgery went well, and I’m in less pain now than before. Instead of working on 3 or 4 tasks a day, I’m just working on 1 at least for the next week or so. So there may not be another update here until next week.

Volatility

The volatility in the equity market has picked up rather dramatically over the past couple of days, with markets falling sharply on Friday and Monday and rebounding Tuesday and Wednesday sharply. In the end, not much has been accomplished. Much of this was expected, as the markets were overbought on an index and individual stock level last week. Additionally, gamma levels reset with the expiration on Friday. None of this should have come as a surprise to anyone.

The question we always ask is, what happens now? It is a tricky one to answer as I think the market is in the midst of transitioning. There is hardly anyone talking about this, but it is clear that something is changing in the market, given the changes in breadth and leadership.

Perhaps this chart illustrates it the best: the 3-month change in the 12-month forward EPS estimates for the S&P 500. The market anticipates changes in EPS growth rates and has successfully done that since the March 2020 lows. However, if you notice, that has changed in recent weeks, and the trend in the growth rate is now sloping lower. If the market is transitioning to a slower growth rate in the future, then it would seem to suggest that the PE multiple should contract and that the current path of the market is to follow that growth rate down.

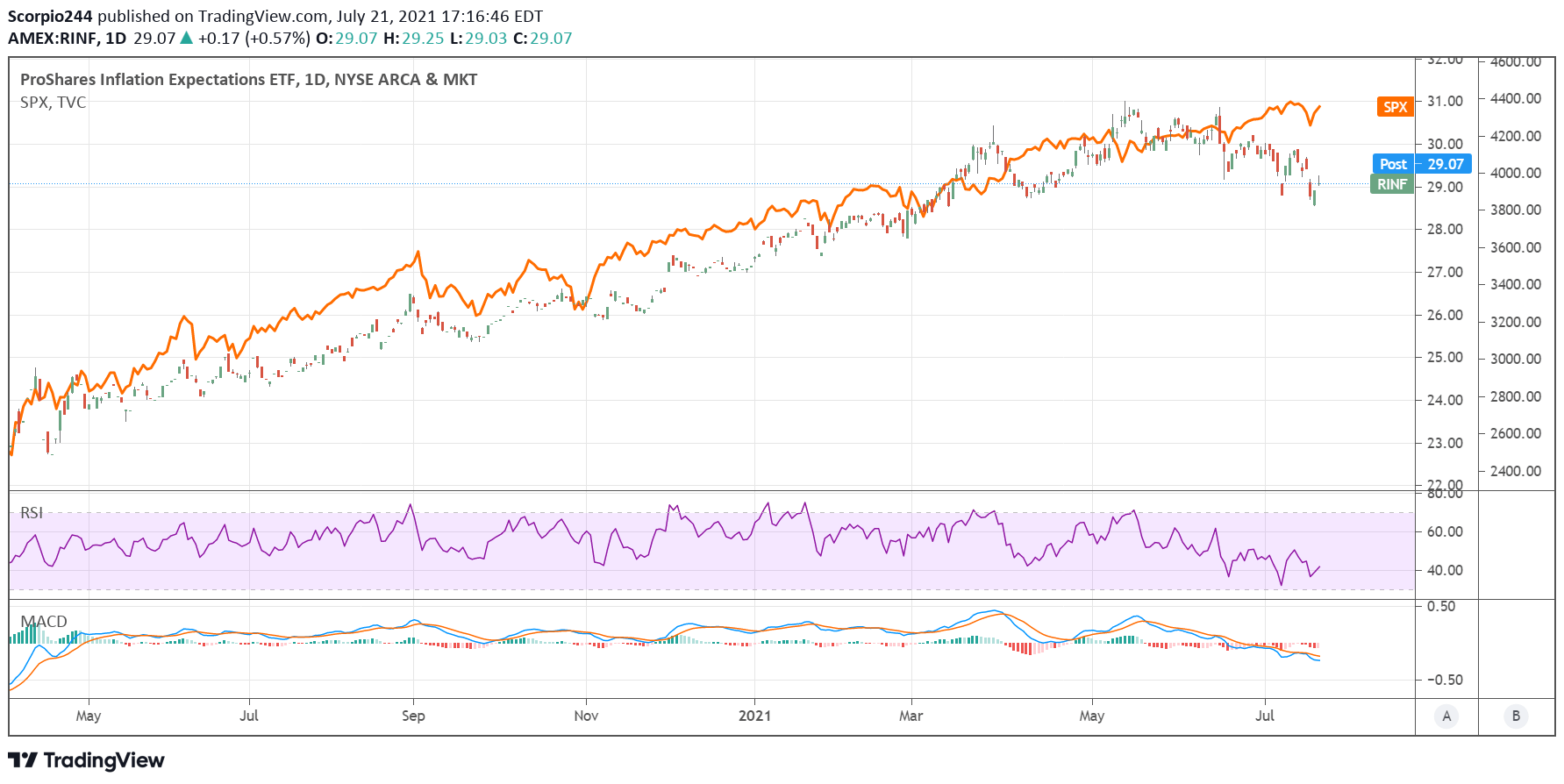

This is not the only thing that is diverging; of course, we have been tracking the divergence between the breakeven inflation expectations and the S&P 500, and that message tells that slower growth lies ahead for the market.

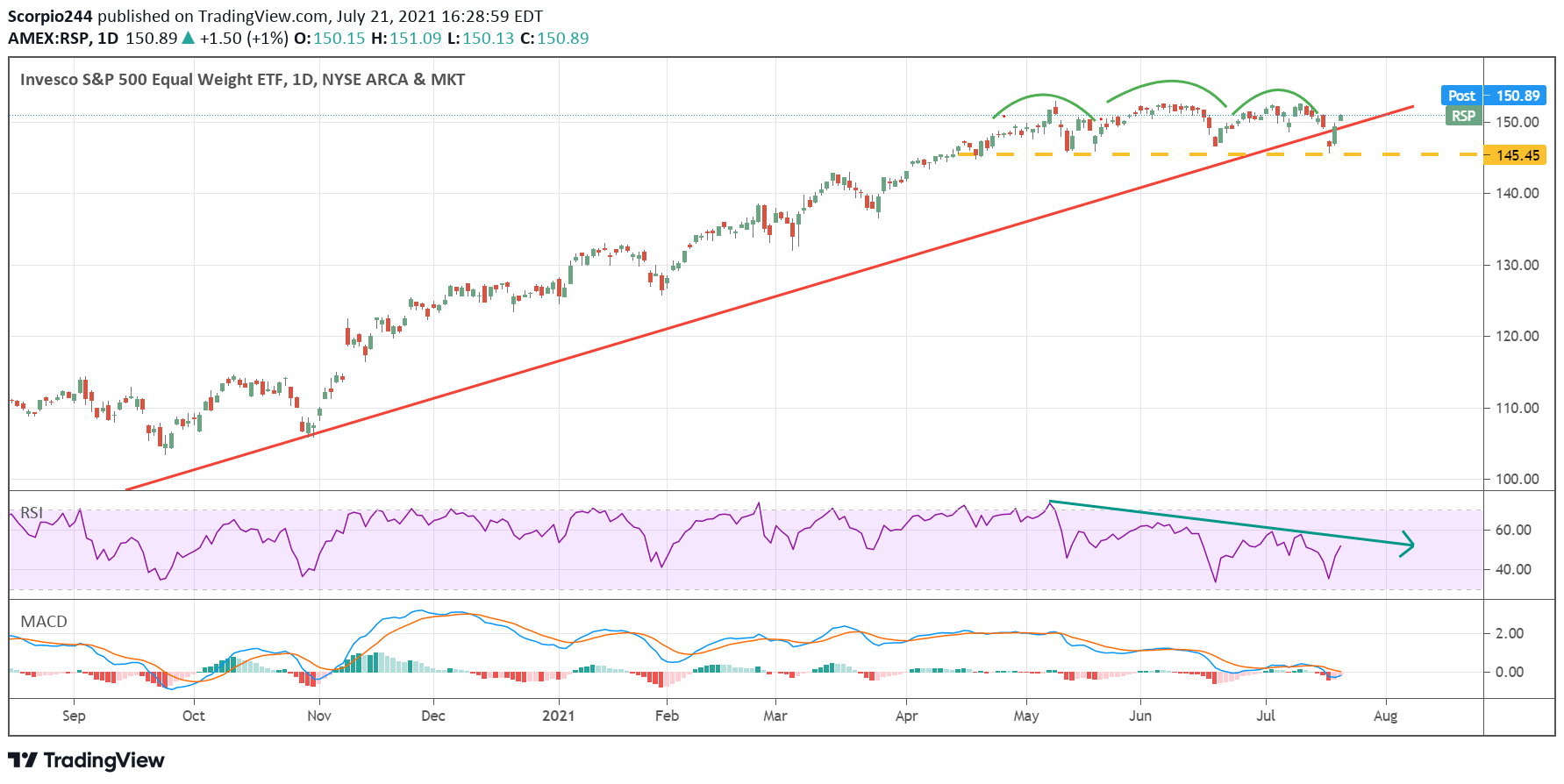

S&P 500 EW (RSP)

The S&P EW (RSP) was a lot of our focus until Wednesday, and it remains in our focus. The RSP has managed to find some key support at the $145.45 level, which was highlighted as support at some point last week. The momentum for the RSP is very negative, and it appears that those negative trends are still a force based on the MACD and the RSI.

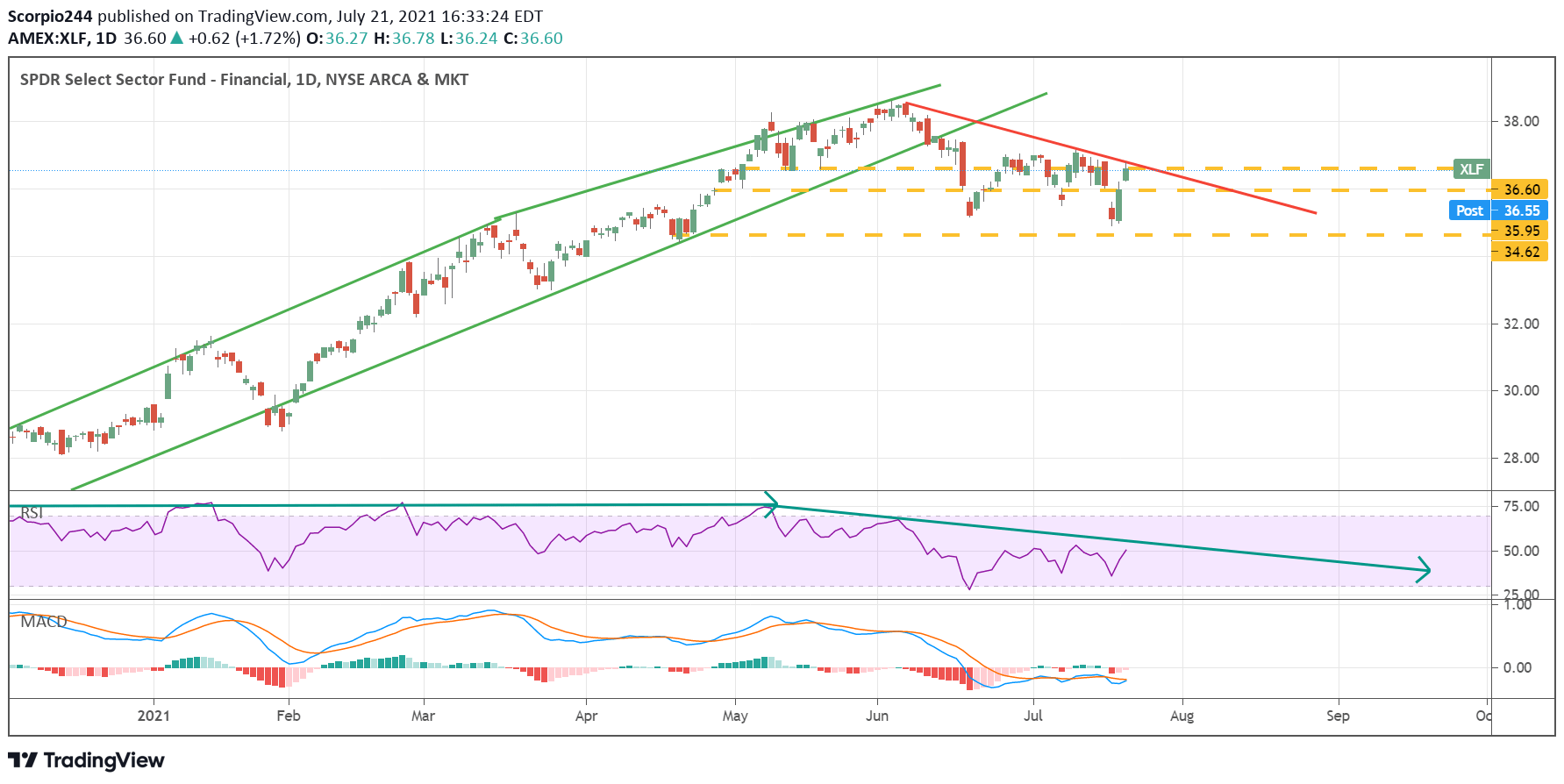

Financials (XLF)

One reason why the S&P 500 has been able to bounce back so quickly is that after falling sharply, yields have moved higher again, which has at least helped lift the reflation trade. The XLF has responded strongly, but finds itself in no better position today than last week, with a negative sloping RSI and overall downtrend on the price level.

Yields

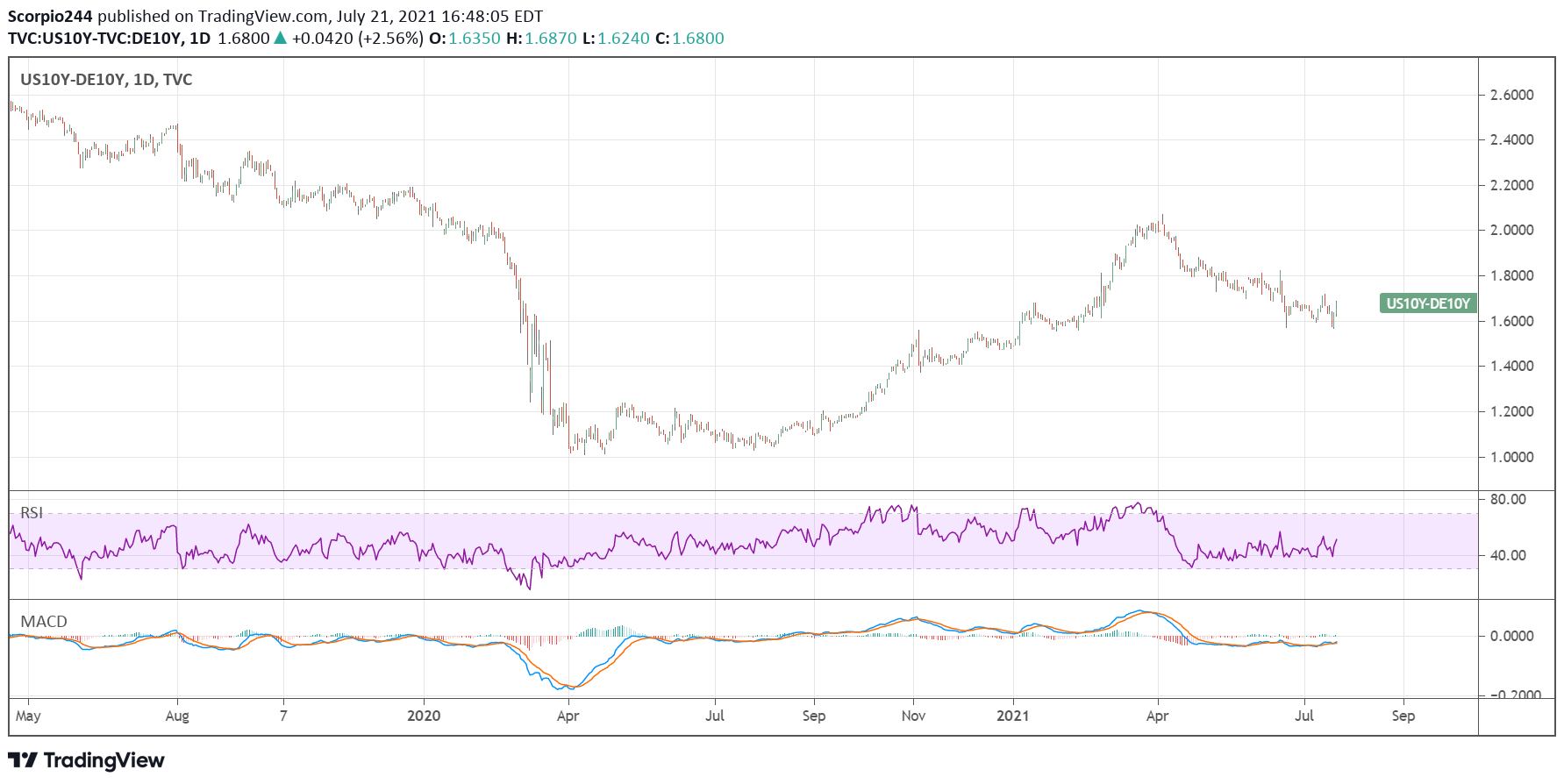

However, it seems unsure to me that yields here in the US will continue to rise. Tomorrow is an ECB meeting, and I expect that the ECB will continue its very dovish monetary policy, if not become even more dovish to help weaken the euro. Overall, the dovish policy of the ECB is what is driving rates across Europe lower, and in turn dragging down US treasury rates too. As long as US rates continue to fall on the long-end, and remain higher on the short-end due to a Fed taper risk, then spreads shall continue to contract, which will continue to send a risk-off message to equity markets. Be aware that tomorrow’s ECB announcement will be significant to how the bond markets respond. If yields in Europe start dropping, it will drag US rates down and push the dollar higher, which could very quickly reverse the equity rebound of the past 2 days.

Mike

Mott Capital Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Past performance is not indicative of future results.