[widget id=”text-22″]

Why Apple’s Stock May Soar By 50% Over The Next 2 Years

MICHAEL KRAMER AND THE CLIENTS OF MOTT CAPITAL OWN SHARES AAPL, GOOGL, V, MA

[widget id=”text-19″]

[widget id=”wordads_sidebar_widget-55″]

Apple’s (AAPL) stock may be too cheap. Shares may be worth up to 50 percent more than the current stock price of $226. That means the stock could rise to $340 over the next two years.

Much of the stock price appreciation will hinge on Apple’s ability to transform from a hardware manufacturer to a services company.

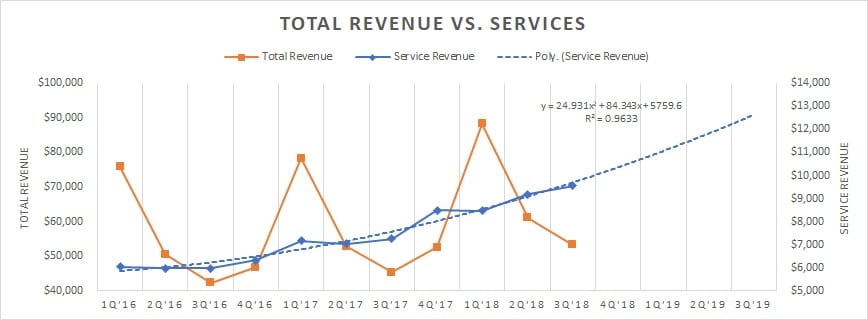

Valuation May Be Too Low

Apple’s stock currently trades at 15 times fiscal 2020 earnings estimates of $15.02. But Apple’s service revenue is growing at a blistering pace. Investors are likely to value Apple’s earnings more over time, willing to pay a higher premium. That’s because service revenue will become a more significant part of total revenue.

AAPL Annual Revenue Estimates data by YCharts

Service Revenue Now #2

Service revenues accounted for almost 18 percent of total revenue in the fiscal third-quarter of 2018, at $9.55 billion. That was Apple second most significant source of income behind the iPhone. The iPhone accounted for 56 percent of Apple’s total revenue of $53.27 billion in the quarter.

Big Growth

Service revenue has risen by almost 60 percent from the third-quarter of 2016 to the third-quarter of 2018. It has also grown on a linear path, avoiding the cyclical nature of iPhone sales. Total revenue would see a benefit of greater service revenue too, becoming more linear as well.

Third of iPhone Sales

Service revenue is growing fast, and it is catching up to iPhone revenue. In the third quarter of 2016, service revenue was almost $6 billion 1/4 of iPhone sales of $24 billion. By 2018 service revenue was 1/3 of iPhone sales. At its current pace, service revenue could rise to about $13 billion in the third-quarter of 2019 and be almost 40 percent of iPhone sales.

Even when looking at the annual results. Service revenue has grown from 11 percent of total revenue in 2016, to 13 percent in 2017. So far in 2018 service revenue through the first three-quarters is about $27 billion. That is almost equal to the $30 billion during all of 2017.

Multiple Expansion

Should service revenue continue to grow as modeled, Apple is likely to trade at an earnings multiple closer to that of some of the consumer discretionary, service-oriented technology, and payment processor companies such as Facebook (FB), Alphabet (GOOGL), Microsoft (MSFT), Visa (V), and Mastercard (MA). That means the stock is likely to trade at an earnings multiple closer to 20 and even as high as 25 times fiscal 2020 estimates. Using the mid-point of 22.5 times 2019 earnings estimates, Apple would be worth about $340, 50 percent higher than the current stock price.

AAPL PE Ratio (Forward 1y) data by YCharts

But for that to happen Apple will need to continue to see service revenue grow at or faster than its current pace. It also assumes the company doesn’t start losing iPhone users, or that other parts of its business do not go into a steep decline.

One thing seems clear. If Apple can continue to deliver stable iPhone sales over the next couple of years, and continue to ramp-up its services business, the stock is likely to continue to rise too much loftier levels.

Subscriber Video’s

Michael Kramer is the Founder of Mott Capital and the creator of Reading the Markets.

2 Stocks To Consider If You Like Square

Big Biotech Breakout, Plus iPhone Super Cycle Maybe This Year!

Biotech And Semis Breaking Out?

[widget id=”text-22″]