Subscribe to receive this daily commentary directly in your email

12.5.20

Stocks – AAPL, AMZN

Macro – SPY

Mike’s Reading The Markets (RTM) Premium Content – NOW WITH A 2 WEEK FREE TRIAL

- The Rising Wedge

- Weak Job Growth Should Revive Double Dip Worries

- VIX Giving A Warning Sign?

- Bearish Trends Mount On DocuSign, As Investors, Await ISM Report – Morning 12.3.20

- Higher Yields Will Crush The Earning Yield Narrative – Midday

- The $200 Million Options Bet – 12.2.20

- The S&P 500 Breaks Out, Uber Is A $90B Food Delivery Co, Zoom Breaks

- Zoom Goes Pop, As The Markets Rock

- Tesla’s Valuation Is Steep. Still Some Think It Has Further To Rise

- Stocks Stuck In Neutral As AMD Surges

- Zoom Earnings, And The Need For Data Analytics – Morning 11.30.20

- One More Push Higher – The Week Ahead 11.30.20

MICHAEL KRAMER AND THE CLIENTS OF MOTT CAPITAL OWN AAPL

Rates rose on Friday to their highest level in some time, with the 10-year closing around 97 bps. It doesn’t sound like much, but consider that the 10-year rate was at 50 bps on August 4, and you can quickly realize that is a pretty big move. Rates could be heading even higher, with stimulus likely coming soon.

The 10-year yield recently broke a downtrend that has been in place since late 2018. It now has its sites on a resistance level around 1.25%, again a very low level based on historical trends. Still, when equity prices have adjusted for these low rates, even the slightest move higher from here could easily disrupt the rally.

Navigating The Market · By Michael Kramer

Independent macro and options research, published every trading day.

Daily written analysis covering gamma exposure, dealer flows, key levels, and the macro drivers moving markets. Includes full video access.

Recent Subscriber Analysis

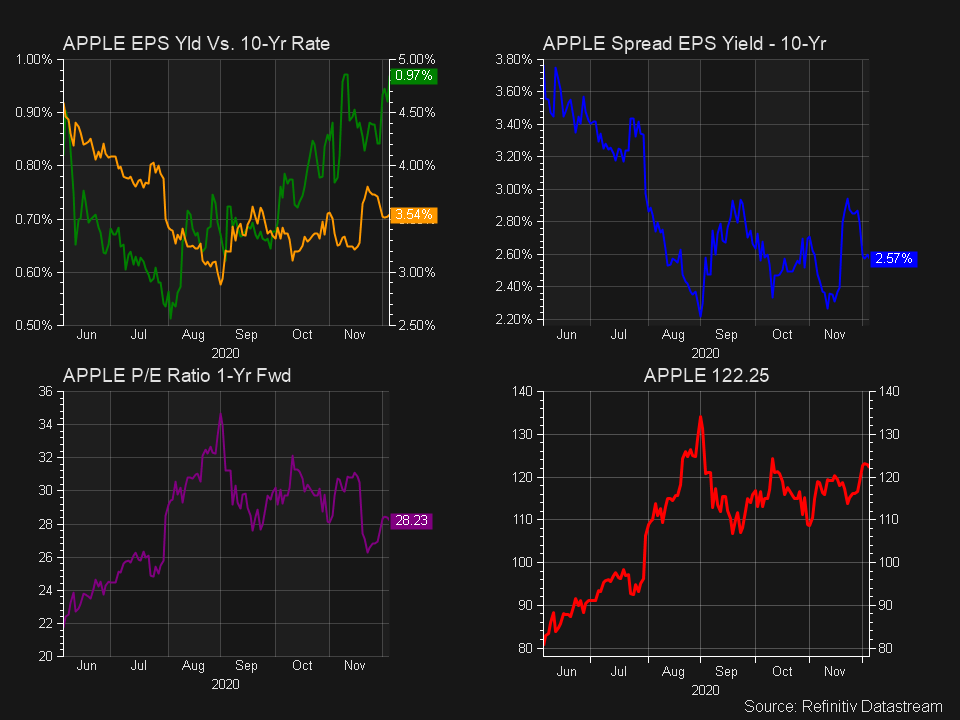

The red line in the chart above and below represents a multi-decade downtrend that has been present in the 10-year rate since 1988. What happens when we reach that trend line is a story for another day.

The big problem is that many stocks have seen their stock prices soar on low rates, dragging their cash flow and earnings yields down to account for the low rate environment. It means that as rates on Treasuries rise, the earnings and cash flow yields for some of these big long-term growth stocks will need to adjust higher as well, which means a lower stock price.

The earnings yield is simply the earnings or earning estimates divided by the stock price. Essentially the inverse of the P/E ratio, another reason we have seen PE ratio soar across the spectrum of equities.

Apple is just one example, with its earnings yield falling to 3.54% this year, its lowest level in years. It simply means that its PE ratio has risen to its highest level in years. The 10-year plunging has driven the move lower in the earnings yield.

In the middle pane, we can see that the spread or the difference between the 10-year rate and Apple’s earnings yield has fallen to 2.57%, its lowest level since late 2015. However, to keep that spread constant, to adjust for rising rates, the stock price will need to fall, or earnings growth will need to accelerate.

The Market Chronicles · Video Membership

The daily market commentary, delivered in video.

Same daily market analysis, in video form — available to YouTube channel members only.

Latest Videos

MegaCap Options Positioning Preview

Rising Real Rates Do The Tightening - Advanced Topics

Rates Are Rising Globally As Dollar Breaks Out, and Stocks Sink

Apple’s stock peaks on September 2 and the 10-year has been trending higher since. Notice Apple’s stock hasn’t advanced; it has been essentially trending sideways.

Meanwhile, notice that in recent days, the spread between Apple’s earnings yield and the 10-year has contracted some, as the price of the stock has risen. But if the yields continue to rise, for that earnings yield to rise, the price of Apple’s stock will need to fall to keep the spread constant; otherwise, the spread will need to contract further, which is possible.

Amazon’s is more of a free-cash-flow yield story since earnings are anything but predictable for the company. The free cash flow yield has also followed the plunging rate on the 10-year.

Again, as rates rise, that free cash flow yield is likely to rise as well, which will be reflected by the price of the stock falling.

So it makes paying attention to the 10-year rate perhaps more important than ever.

-Mike

Mott Capital Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Past performance is not indicative of future results.

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.