Subscribe to receive this daily commentary directly in your email

MICHAEL KRAMER AND THE CLIENTS OF MOTT CAPITAL OWN TESLA

[widget id=”text-19″]

Bond markets are closed on Monday, November 12 for Veterans Day. Then on Tuesday, we get a critical CPI inflation reading. On Wednesday, FOMC Chairman Powell will speak. Both CPI and Powell will likely catch the attention of equity investors this week.

Rally?

Despite the steep sell-off in equity prices on Friday, the past week was reasonably healthy. The S&P 500 rose by more than 2% and is now more than 5% off its October 29 lows. Certainly, the equity market today is in a better place than two weeks ago, when it felt like a bottom was nowhere in sight. Can we continue to rally between now and year-end?

Strong Results

With about 90% of S&P 500 companies now having reported earnings, 77% have topped earnings estimates, while 16% have missed, and 7% have met. Certainly not as strong as the second quarter showing, with 80% beating, 15% missing, and 5% meeting.

Although the number of companies beating estimates fell this quarter, the good news is that it is not because they missed. Instead, we saw the most significant uptick in the “met” category. Hard to say this quarter has been a disappointment based on this information.

Increasing Estimates

Even more interesting is that operating earnings estimates for 2018 have risen since the end of October to $158.26 from $157.39. Earnings estimates for 2018 have increased by 8.5% since the end of 2017.

Slowing Growth

One concern, if it is a concern, is that there is a trend of earnings estimates for 2019 now starting to fall. Since August 23, earnings estimates for 2019 have dropped by 1% from $177.07. With 2019 estimates falling and 2018 estimates rising, it has resulted in the earnings growth in 2019 dropping to 11% from 12.2%

Make no mistake 11% earnings growth for next year is still strong. Still, it is the trend for 2019 that must concern us. Should growth estimates for 2019 continue to trend lower, it will have a negative impact on the potential for the stocks markets rise next year.

It would seem at this point earnings growth is being pulled forward into 2018 at the cost of 2019 results. While it is good for 2018, it may also mean that we have pulled forward the stock markets returns into 2018 at the expense of 2019.

Again, we need to continue to watch this.

Margin Expansion

One thing that I do find interesting is that all of this “talk” of rising wages and rising “cost” has certainly had no impact on operating margins in the third quarter. That is because margins have increased to their highest levels in years to 12.2%. That is 200 basis points higher than previous cycle highs in 2014 and 2016.

Navigating The Market · By Michael Kramer

Independent macro and options research, published every trading day.

Daily written analysis covering gamma exposure, dealer flows, key levels, and the macro drivers moving markets. Includes full video access.

Recent Subscriber Analysis

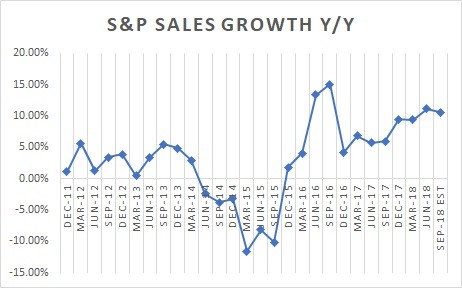

The good news is that strong earnings growth is not only coming from strong margins. It also happens to be the strongest sales growth in years rising to $341 per share a 10.6% year-over-year increase and almost 2% sequentially growth.

The higher cost companies are seeing may very well be a headwind for next year and lower margins. Given the tremendous amount of margin expansion this year, it seems nearly impossible to continue, and that may be the primary reason earnings estimates for next year are starting to fall. But again one or two percent is not earth-shaking, but should it become 5 or 6%, then it will become problematic. So still, we will need to continue to watch these trends over the next few weeks.

In the short-term, can the equity market continue to recover over these next few weeks, yes most definitely. What happens from January to March may very well be a much different story, as more data becomes available.

Facebook (FB)

Lets move on to stocks for the week and lets start with Facebook. The more I think about Facebook and watch it trade the more concerned I get for the stock moving forward. The stock is a train wreck plain and simple. Every time the stock shows the slightest hint of a breakout, sellers come in and push it lower. I think at this point there is no evidence to suggest this trend shall change. I think this stock is heading back to $140 and perhaps lower to maybe $133.

Analysts now estimate Facebook’s earnings in the fourth quarter to drop by 2% from last year. Earnings growth for 2019, and I can’t believe I’m writing this, are forecast to rise by just 1% to $7.54 per share. That is down from the previous forecast in July for growth 17% in 2019.

Even worse, analysts have cut 2020 earnings estimates for Facebook a stunning 19% since July to $8.62 from $10.58 per share.

This stock still has further to fall. When a growth company is not growing, that is terrible news. Don’t be fooled by its 19 PE ratio either; this stock is now expensive.

FB EPS Estimates for Next Fiscal Year data by YCharts

Tesla

Here is an interesting chart. Now I’m not sure if you can use technical analysis on fundamental ratios but we are going to give it a shot with Tesla. I stumbled upon this chart for Tesla of a one-year forward price to sales ratio. Now based on this chart, Tesla’s stock price may be on the verge of a massive rise.

The chart below shows a steady level of support and resistance at 2.9 times forward sales. It also shows the ratio is in the middle of a significant downtrend, which it may now be breaking free from. If that is the case and should forward sales increase to 2.9 times, given sales estimates of $29.11 billion in 2019, the stock may be on the verge of a 40% rise. It would give the stock a market cap of $85 billion or about $500 per share. If it happens, remember you heard it here first!

Amazon (AMZN)

If it is the case and this type of analysis works for fundamentals, then Amazon may still have a bit further to fall, perhaps another 10% or so over the longer-term.

The Market Chronicles · Video Membership

The daily market commentary, delivered in video.

Same daily market analysis, in video form — available to YouTube channel members only.

Latest Videos

MegaCap Options Positioning Preview

Rising Real Rates Do The Tightening - Advanced Topics

Rates Are Rising Globally As Dollar Breaks Out, and Stocks Sink

Nvidia (NVDA)

Nvidia reports this week, and the technical chart still looks terrible. The stock failed at resistance at $217. The RSI is still trending lower with no bottoming in sight.

What has me the most concerned is that analysts have not lowered their estimates at all for Nvidia. I don’t know, maybe Nvidia blows out results, but there haven’t been many chip companies that have blown out earnings this quarter.

NVDA EPS Estimates for Current Quarter data by YCharts

Good Luck this week

-Mike

Mott Capital Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Past performance is not indicative of future.

S&P 500, SP500, NASDAQ, Earnings, tesla, amazon, facebook, nvidia

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.