Subscribe to receive this daily commentary directly in your email

1/15/23

STOCKS – $NFLX $GS $PG $JPM

MACRO – $SPY, $VIX,

Mike’s Reading The Markets (RTM) Premium Content – $70 per month or $600 per year – GET 20% OFF!

- RTM: Here Comes Another Options Expiration Date

- RTM: S&P 500 Faces A 6% Drop

- RTM: Earnings Season Starts Tomorrow

- RTM: The Market Is Priced For Inflation Perfection

There will be a lot of data this week, and perhaps more critically, Lael Brainard speaks on Thursday. Now, typically Jay Powell is the most important when it comes to Fed speakers. But Brainard is the Vice-Chair, and while Powell is the Chair of the FOMC and the committee leader, Brainard is the leader of the Doves on the committee. This week’s speech and Q&A session are essential because it comes on Thursday, the day before the Fed enters a blackout period. If she signals the same hawkish stance as many of her colleagues and talks about getting rates to 5% and holding rates high for some time, then I think it kills any hope the market has of the Fed not reaching the path laid out in the dot plot or cutting rates in late 2023. If she gives a dovish speech, I think you will see the market continue to rally.

If the rally is going to end, it will be this week, Brainard’s speech being enough. Another reason this week could kill the rally is that this week is options expiration week, and at least as of Friday, the big gamma level was at 4,000, and the level with the most call gamma was also at 4,000. As long as that remains, the index will likely stay pinned at 4,000 and not drift much further. Could it go to 4,025? Sure. Is it likely to go much higher? Probably, not unless the options market gives the S&P 500 permission to go higher, and for that to happen, the gamma level with the most call concentration needs to move higher to 4,100.

Additionally, the Treasury General Account has been drifting lower recently, adding liquidity to the market and allowing reserve balances to rise. Typically speaking, the TGA tends to increase mid-month following the settlement of Treasury auctions, which could lead to the TGA rising this week, which could act to lower bank reserves and drain liquidity from the market.

Navigating The Market · By Michael Kramer

Independent macro and options research, published every trading day.

Daily written analysis covering gamma exposure, dealer flows, key levels, and the macro drivers moving markets. Includes full video access.

Recent Subscriber Analysis

- Credit Keeps Repricing The AI Complex As The Market Rotates From Semis Into Software

- MegaCap Options Positioning Preview

- Rising Real Rates Do The Tightening - Advanced Topics

- Rates Are Rising Globally As Dollar Breaks Out, and Stocks Sink

- NVIDIA Props Up The Index While CDS Spreads Widen Across The AI Names

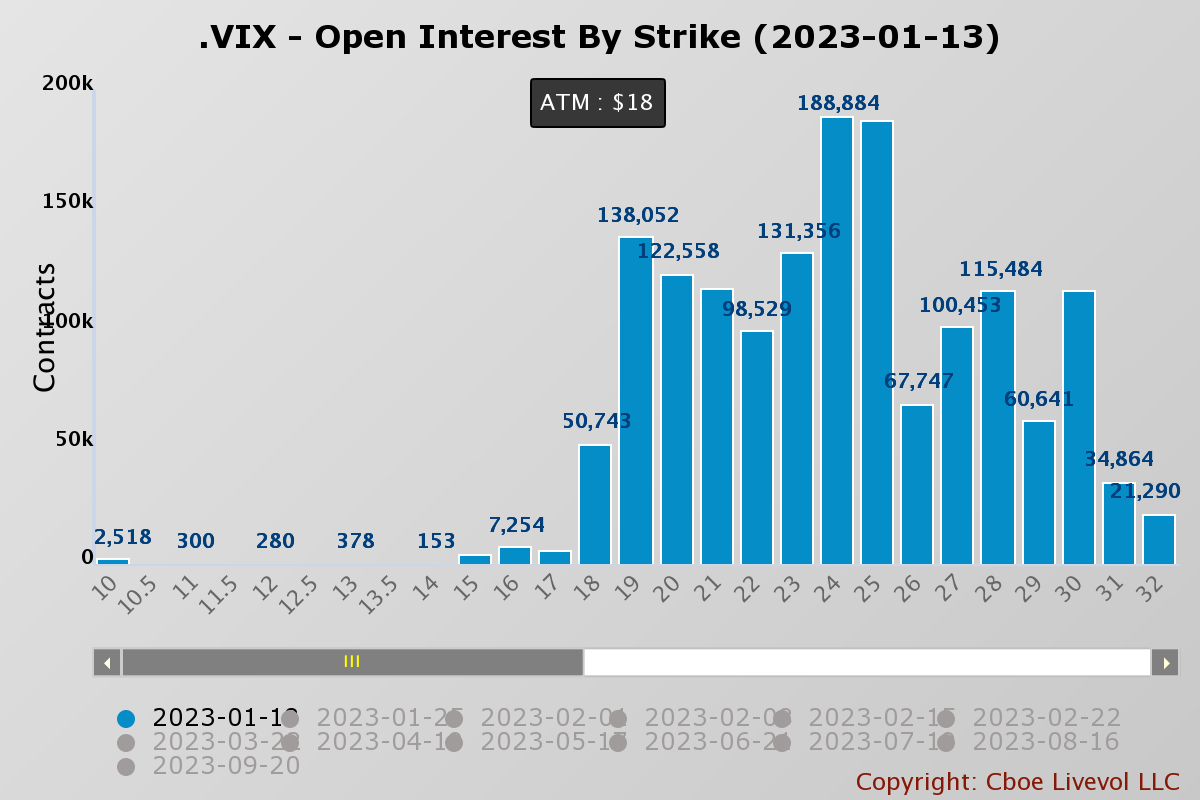

Additionally, there will be a VIX options expiration this week, and there aren’t many options with open interest below 19 on the VIX. This means there will be many call options that will expire worthless if the VIX stays in the 18 range heading into OPEX.

But more importantly, we see the VVIX begin to move higher again as the VIX moves lower. Typically, when the VIX to VVIX ratio is rising, it is accompanied by a market that is falling, and when the VIX to VVIX is falling, it is accompanied by a market that is rising. In this case, the VIX to VVIX ratio is near a low point, which means the VVIX is starting to rise relative to the VIX, which tells us the S&P 500 is nearing a top.

The Market Chronicles · Video Membership

The daily market commentary, delivered in video.

Same daily market analysis, in video form — available to YouTube channel members only.

Latest Videos

Credit Keeps Repricing The AI Complex As The Market Rotates From Semis Into Software

MegaCap Options Positioning Preview

Rising Real Rates Do The Tightening - Advanced Topics

S&P 500 (SPY)

Meanwhile, the S&P 500 is within a bigger broadening wedge similar to the one seen in August, and like in August it is hitting up against its long-term downtrend. It also filled the technical gap at 3,995. All conditions suggest we could see a similar outcome to that in August. Again, this is the week that the index should turn lower if we are still in a bear market.

Banks

Meanwhile, the big banks reported results on Friday, and I thought they were ok, nothing special. What is more telling than the stocks moving higher is how the CDS traded, and while the stock prices went higher, the CDS for JPMorgan, Bank of America, and Citigroup saw their CDS all increase just a bit.

Typically the CDS and equity trade opposite one another, meaning if the CDS rises, the stock prices fall and vice versa. In this case, the stock rose, and the credit default swap rose on Friday. This means that one of the two is wrong; if I had to guess which one is wrong, my guess would be the equity market.

The reason is that implied volatility was crushed on Friday in these stocks, and JPMorgan, for example, saw its IV fall 30.7 to 16.1. If the stock gives back Friday’s gain next week, it probably confirms this idea.

Goldman (GS)

I will be curious this week to see how Goldman Sachs numbers are given how much this stock is up over the past couple of months. The company will report results Tuesday morning, and the shares are approaching an overbought level on the RSI and resistance at $375, where they failed on December 13. Additionally, the short-selling volume has steadily risen over the last few days.

Procter & Gamble (PG)

Procter And Gamble will report on Thursday morning, which will tell us a lot about inflation and margin impacts, whether the company can still pass on the higher cost to its end customers or not, and what the effects are on gross margins as a result. The stock has a bearish RSI trending lower and appears to have a potential triple pattern, with a move below $148 setting up a possible decline to $141. Short sales volume for PG has been rising as well in recent days.

Netflix (NFLX)

Netflix will report results on Thursday, and I don’t have a feel for this one like I used to. I never expected this stock to rally as much as it has. The gap from April 2022 is filled, and the RSI is overbought. So if this stock is going higher, these results will be necessary to support the bullish thesis. If the downtrend is still intact and the gap is filled, it should reverse lower; if a new uptrend has been established, it probably rallies back to $360.

See you next week.

-Mike

Charts used with the permission of Bloomberg Finance LP. This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Past performance of an index is not an indication or guarantee of future results. It is not possible to invest directly in an index. Exposure to an asset class represented by an index may be available through investable instruments based on that index. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.